I've been having writer's block for the past three weeks as I've been trying to sit down and write my 2009 economic outlook. While in normal years, I could assess the state of the business cycle, look at asset prices and make a call. This year, however, we are caught in a web of epochal changes on par with the 1930s and 1940s or the 1860s and 1870s. The entire global economic system is threatening to break down, and for good reason. Since World War II the world has relied on the relentless increase of US consumer demand. The increase in US consumer demand has been driven by a relentless increase in US consumer indebtedness. Both of these forces have been deliberately fostered by US economic policy. Not surprisingly, US economic policy has been driven by the lessons learned in the Depression and articulated by two economic schools of thought, Keynesian and Monetarist. The Keynesian school articulated that the government should step in to fill the void in private demand during recessions. The Monetarist school posited that the central bank should step in to prevent a contraction in credit, and by extension the money supply, during downturns. Since the Depression both methods have been used liberally to fight recessions, mostly successfully, but have also been bastardized for political ends. The Keynesians have used policy to not only temporarily support demand during downturns, but to also promote permanent increases in consumer demand, particularly through the promotion of housing and consumer spending. The Monetarists have used policy asymmetrically, supporting credit during downturns but letting booms run unabated. As a result, dangerous imbalances have built up.

The other theme for the past 60 years has been the relentless expansion of the financial sector, first from absurdly low levels after the beating it took during the Depression and the New Deal, then into the massive expansion of the past 30 years. There has been a great deal of innovation in the financial sector, making the US the most efficient allocator of capital in the world. The financial sector has also become dangerously unstable and has magnified the global boom and bust cycles of the past 30-40 years. A series of constantly shifting imbalances has ruled the global economy during this time. Much of this instability has been tolerated because, for the most part, it has been during a virtuous cycle of rising global living standards supported by the US's willingness to lever itself up. Now that the cycle may be turning vicious, we could be in for 10-20 years of serious global crisis if world leaders don't get together to restructure the world economy. Until it becomes clear that such a change is occurring, caution will be the proper stance.

Because of the momentousness of the trend changes underway, I have been forced to break up my analysis into several parts. Part I will set the context of how today's economic policy mix was shaped by the Depression. Part II will discuss the US trade deficit and indebtedness. Part III will discuss consumption and investment and the sources of GDP growth. Part IV will discuss the dollar and inflation. Part V will be a policy manifesto for the new era.

Part I – The Depression's Long Shadow

The effect of the Depression on policy today

There has been a great deal of commentary that has compared today's situation to that of the Great Depression. There are similarities. First, there is the great debt overhang that has built up, resulting in the threat of debt deflation. Second, we are in similar position in the Kondratiev Cycle, moving from the good disinflation to the bad disinflation phase (if you believe in that sort of thing, which I actually do). There is also the high wealth disparity that has built up over the course of a long bull market and the obvious switch from a Republican-dominated government to a Democratically-dominated one.

There are big differences, however, as well. The US's macroeconomic position is much different now than it was at that time. During the early 1900s the United States was in a position more similar to Japan in the 1980s or China today. It was a rising, mercantilist power that ran big trade surpluses and was a net creditor to the rest of the world. It had a relatively small government sector that did not greatly interfere in the private economy. The government had long run balanced budgets and was historically tight-fisted. Most government revenue came from protective tariffs and the use of income taxes was limited. The US had a huge amount of excess production capacity that sat idle when domestic demand was insufficient to take up the slack after world trade collapsed in the Depression. The US was on the gold standard and value of the dollar had remained unchanged vs. gold at $20.67 since the revolution (with blips during major wars), even though the economy had grown many times over, and up to the start of the Depression the general price level was basically the same as it had been in 1800. It is also important to note that debt to GDP wasn't that high at the beginning of the Depression (it went from 140% of GDP at the beginning of World War I to 160% by the end of the 1920s), it was only after a massive collapse in the economy and debt deflation that it rose to 250% of GDP by 1933, as shown here. It was as the economy shrank faster than the nation's debt load, that the ratio of debt to GDP rose.

The policies of the New Deal were designed to correct some of the imbalances that had built up over the previous 70 years. In the era prior to the Great Depression, the core economic policies of the United States were designed to encourage manufacturing production. The primary form of tax was the protective tariff, which encouraged domestic production and taxed consumption of imports. Large trusts were formed to limit domestic price competition. To counter the pressure on laborers' wages, from competition in the 1920s the government passed highly restrictive immigration laws. World War I, however, had thrown the rest of the world system into chaos. During the War, the US lent large sums of money to its allies, which it could then in turn use to by US-manufactured war materiel. The US thus ran very high trade surpluses and built up a stock of European capital. After the War, the allies began to repay their loans, sending money back into the United States. As the money flowed back into the US banking system, it was lent out and supported the great production, consumption and asset boom of the 1920s. When it ran too far, it began to collapse into a classic debt deflation. As domestic demand retreated with the supply of money and credit, the US government tried to keep the party going the only way it knew how: by raising tariffs to support domestic industry, raising taxes to keep the budget balanced, and keeping interest rates high to protect the gold standard.

In not doing those things you get the three US ideologies of the Era since the New Deal: free trade Globalism, Keynesianism and Monetarism.

We encourage open world trade, even if other countries manipulate our willingness to do so with mercantilist policy. We use government policy to encourage increasing domestic demand: deficit spending, policies that support consumption at the expense of saving and investment, and policies that encourage borrowing money to buy houses. We manipulate the money supply to support ever-rising indebtedness and prices.

The policies of the New Deal were appropriate for the situation the country was in then. Reduce the value of dollar to fight deflation. Establish the SEC to increase investor confidence. Establish the FDIC to prevent bank runs. Establish home loan banks to support housing prices and financing. Break up the highly concentrated financial system to reduce risk. Use government money to invest in infrastructure when private investment demand dried up. Establish Social Security and unemployment insurance to reduce consumer risk so they consume more. Encourage unions to fight for higher wages. Use the progressive income tax to tax the large pool of savings at the high end to support policies that help lift domestic demand. Encourage investment in rural areas. Be (somewhat) willing to run government deficits to support demand when private demand is not present.

The road to excess

These policies all made sense at the time and most still do. The problem is that the constituencies that support these policies became more powerful as time moved on and the policies have gotten pushed too far. Even now, when it is obvious that as a nation we need to save more and spend less, that we have too many houses relative to demand, that we consume more than we produce, that our debt level has risen to 350% of GDP from 150% as recently as 1980, that we have seen our currency fall 98% vs. an ounce of gold since FDR took office…what are we doing? We are seeing our policymakers insist that the cure lies with policies that spend money we don't have, try to support housing prices, try to encourage more consumption, try to encourage more lending and borrowing and devalue our currency further to maintain a positive level of inflation. Let me use pictures to drive the point home:

How does a country whose demand exceeds production by 5% of GDP suffer from a lack of demand?

Why should over-indebted consumers be encouraged to keep consuming?

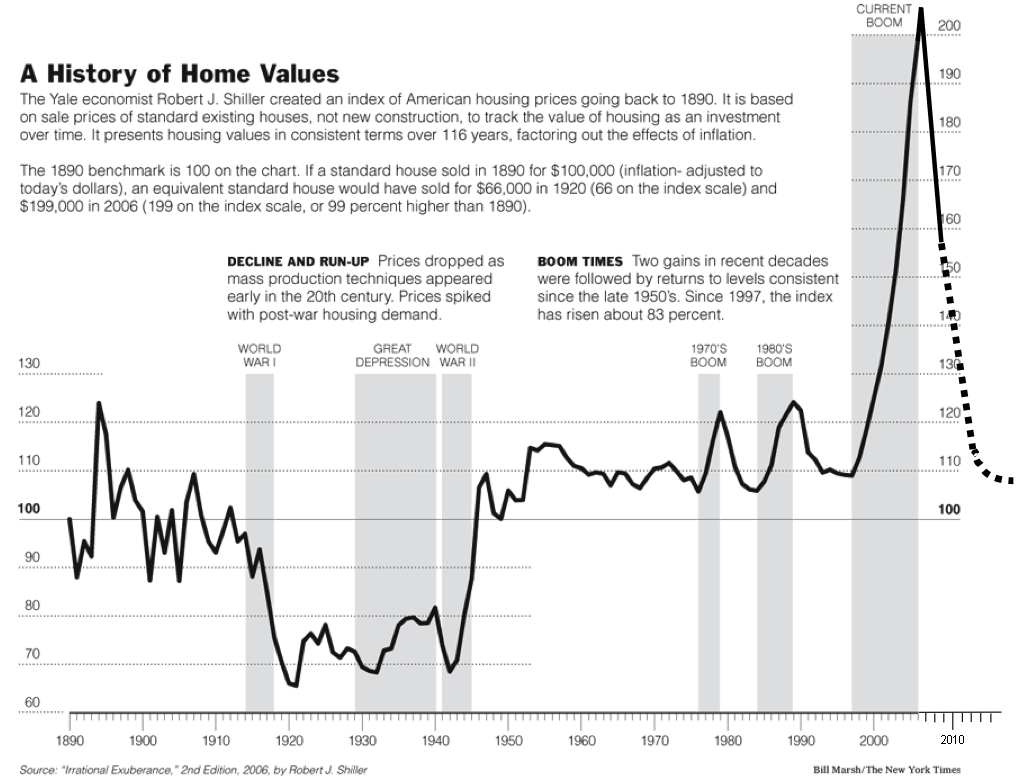

How exactly are we supposed to support home values when they are still 30% above their long term trend?

How does a country whose currency has lost 95% of its value relative to gold in the past 40 years have a deflation problem?

What the current situation means for policy makers

In an effort to prevent near term collapse, we are doing exactly the opposite of what we need to do as a country to get ourselves out of our mess. Instead, we are fighting, spending literally trillions of dollars, just for the privilege of staying in the mess we're in. It is madness.

We need to balance our policies to reverse or halt these trends. We need policies that:

- Improve the terms of trade for the US to run a trade surpluses or a neutral trade deficit

- Encourage domestic saving at the expense of consumption

- Roll back policies that favor residential investment at the expense of business investment

- Encourage a sound dollar, zero to low inflation, and a sound, stable financial system

Because these are the types of policies that exacerbated the Great Depression, they are despised by the elites that learned about the Great Depression in graduate school. It is no longer fashionable to study the period between the Civil War and the Great Depression, even though in many ways it was America's economic golden age. I would argue that cyclically, today we are in a period more similar to the depression of the 1840s, after Andrew Jackson's experiment with wildcat banking (read paper money and hedge funds), Manifest Destiny and the yeoman farmer (read real estate speculation), and low tariffs, open immigration and the support of large-scale agriculture and mining. Out of this collapse would rise the northern-based Republican Party, which favored sound money, internal improvements and infrastructure investments, high tariffs, restricted immigration, the support of manufacturing, and, oh yeah, the abolition of slavery. The blueprint for success is there for the taking.

Excellent start, Tyler. Can’t wait to see the rest. I’ve got thoughts about trade imbalance and the religion of bolstering currency strength, but will wait for Part 2…

LikeLike

Why is it taking so long for the media, economic and political analysts to just say the words already. We are in a depression. I know people are afraid of mass panic and making things worse than they already are, but for crying outloud, it’s here we all know it so let’s deal with it head on and quit mincing words.

LikeLike